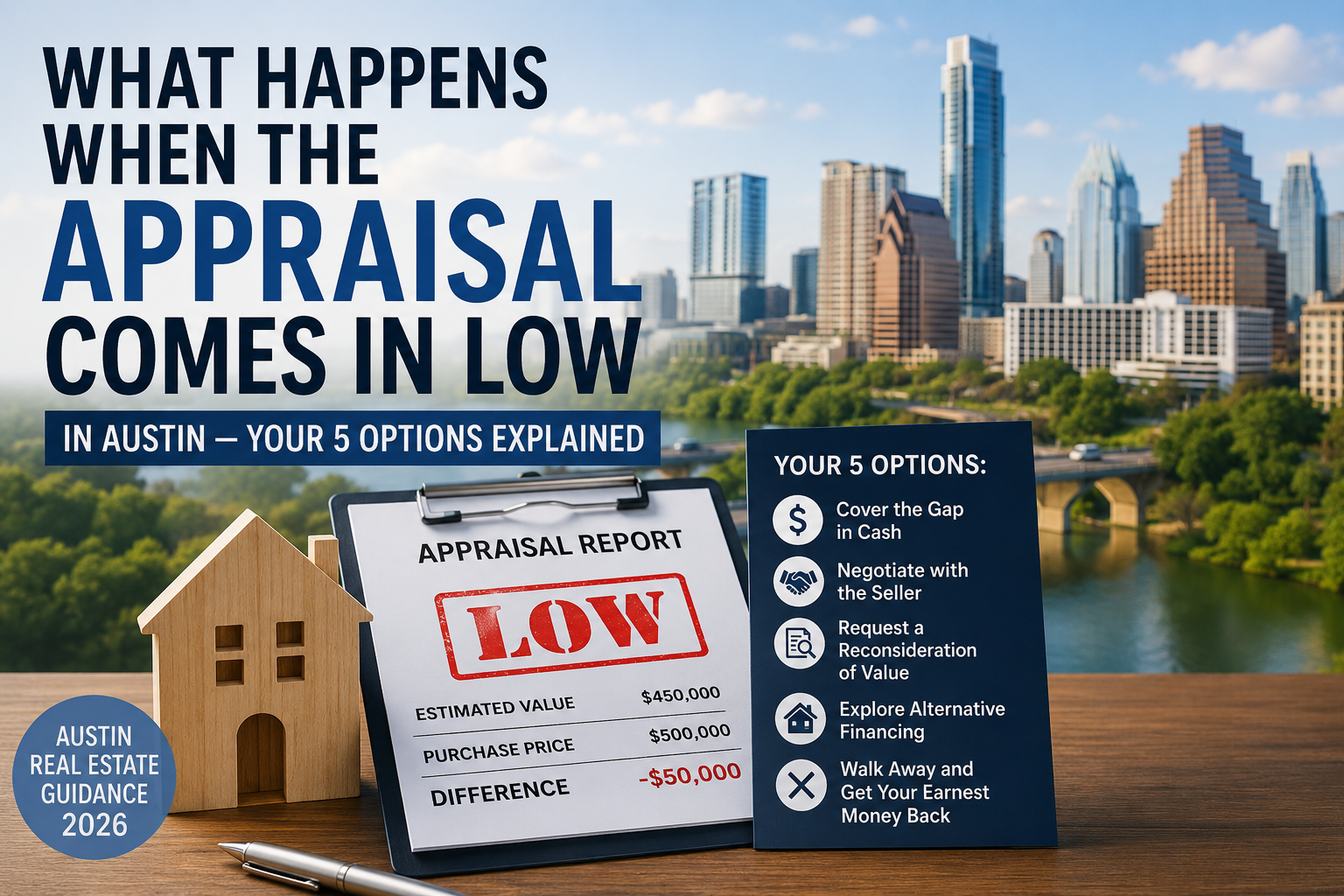

What happens when a home appraisal comes in low in Austin, Texas?

When an appraisal comes in below the purchase price in Austin, the buyer has five options: pay the difference in cash, negotiate with the seller to reduce the price or split the gap, request a Reconsideration of Value, terminate the contract under the financing contingency and recover their earnest money, or invoke an appraisal gap coverage clause if one was included in the offer. In Austin’s 2026 buyer’s market — with 6.0 months of inventory and sellers actively negotiating — price reductions after low appraisals are common, and sellers often have limited leverage to push back.

You made the offer. It got accepted. The inspection went smoothly. Then the appraisal report came back — $25,000 lower than your purchase price. Your lender calls. The deal is suddenly at risk. Now what?

A low appraisal is one of the most stressful moments in a real estate transaction, and it’s happening more often in Austin than most buyers expect. Here’s exactly what it means and what your five options are.

Why Low Appraisals Are More Common in Austin Right Now

The Austin real estate market has shifted significantly since the 2022 peak. Travis County median home values are down 15.91% from their May 2022 high. Appraisers use recent sold comparable sales to establish value — and in a market where prices have pulled back substantially, appraisals are more likely to come in below what some sellers still hope to get.

Here’s something buyers often don’t realize: the appraiser works for your lender, not for you. You pay for the appraisal (typically $400–$600 in Austin), but the appraiser’s job is to protect the lender’s collateral — not to validate the price you agreed to pay. If the appraiser determines a home is worth $475,000, your lender will only finance up to $475,000, regardless of what your contract says.

That gap between the appraised value and the purchase price has to be resolved before your loan can close. With 50% of active Austin listings showing price reductions and 6.0 months of inventory putting real power in buyers’ hands, you have more options than you might think. Understanding where Austin’s market stands right now is the context that makes all five options clearer.

Your 5 Options When the Appraisal Comes In Low

Option 1: Cover the Gap in Cash

You can proceed with the purchase by bringing extra cash to closing. If the purchase price is $500,000 and the appraisal comes in at $475,000, you cover the $25,000 difference out of pocket — on top of your down payment and closing costs.

This option makes sense when you believe the home is genuinely worth the purchase price, you have the cash reserves to absorb the gap, and you don’t want to risk losing the home through a renegotiation that might not go your way. Before committing, make sure you have a clear picture of every cost you’ll be bringing to closing so the appraisal gap doesn’t blindside your budget. Covering the gap in full is less common in 2026 than it was in 2022, but it remains the cleanest path when the numbers work for you.

Option 2: Negotiate with the Seller

This is the most common resolution in Austin right now. When the appraisal comes in low, your agent presents the report to the seller and opens a negotiation. The seller can agree to lower the purchase price to the appraised value — or you can meet somewhere in the middle and each absorb part of the gap.

In a market with 6.0 months of inventory, 50% of listings with price reductions, and an average of 54 days on market, sellers who push back on a low appraisal face a clear-eyed reality: losing you means starting over. And starting over in this market usually means accepting a lower price from the next buyer anyway. The data is on your side. Your agent’s job is to present it calmly and let the market logic do the persuading.

Don’t assume the seller will walk. Most don’t — not when the alternative is another month or two on market followed by the same conversation with a different buyer.

Option 3: Request a Reconsideration of Value

If you and your agent believe the appraiser overlooked relevant comparable sales — especially recent ones — you can submit a formal Reconsideration of Value (ROV) request through your lender. Your agent compiles the supporting comps, your lender submits them to the appraiser, and the appraiser reviews whether to revise the value.

ROV requests work best when there are specific, legitimate comparables the original appraisal missed: a recently closed sale in the same neighborhood at a higher price per square foot, or a comparable property with fewer upgrades that sold near your purchase price. Appraisers have discretion and aren’t required to revise their conclusions — ROVs succeed in a minority of cases. But when the data is genuinely there, it’s worth pursuing.

This path adds 1–2 weeks to your timeline and requires lender cooperation. Your agent will know quickly whether the comparable evidence is strong enough to make the case.

Option 4: Terminate Under the Financing Contingency

Texas real estate contracts include a Third Party Financing Addendum — standard TREC language that gives you a financing contingency. If the home doesn’t appraise at value and you’re unwilling or unable to cover the gap, you might be able to terminate the contract within the financing deadline and receive your earnest money back.

The financing deadline is typically 21–30 days after contract execution, so you’ll know the appraisal outcome before that window closes in most cases. This is a clean, legal exit — you lose no money, and the seller returns to market. It’s also a good reason to know exactly what to ask before you make an offer, including whether a property’s pricing history suggests appraisal risk going in.

In Austin’s current buyer’s market, walking away from a property with a significant appraisal gap is a reasonable, well-protected decision. There are other homes. The market isn’t punishing buyers for being disciplined right now.

Option 5: Invoke an Appraisal Gap Coverage Clause

An appraisal gap coverage clause is language written into your original offer that pre-commits you to covering a gap up to a specified dollar amount. Example: “Buyer agrees to cover any appraisal gap up to $15,000.” During Austin’s 2021–2022 seller’s market, these clauses appeared in roughly 60% or more of competitive offers — buyers were determined to win and willing to absorb risk upfront to do it.

In 2026, only about 15–20% of Austin offers include appraisal gap clauses. Buyers simply don’t need to offer them anymore. But if your original offer included one and the gap falls within your stated cap, you’re committed to honoring it. If the gap exceeds your cap, you’re back to negotiating or terminating.

If you’re preparing to make an offer and wondering whether to include an appraisal gap clause, the honest answer in this market is: you probably don’t need one. Your agent can advise you based on the specific property and the competitive situation at hand.

What Happens Next — and How Fast You Need to Move

Once the appraisal report is in, you and your agent need to move quickly. Your lender is waiting on a resolution before they can proceed with final underwriting. If you’re pursuing a price reduction, the amended contract needs to get executed promptly. If you’re going the ROV route, your financing deadline is still ticking.

Keep your lender in the loop at every step. Any change to the purchase price requires a loan amendment, and your lender needs time to process it before your closing date. The buyers who navigate low appraisals most smoothly are the ones whose agents, lenders, and sellers’ agents are communicating clearly and quickly — not the ones who wait and hope the problem resolves itself.

A low appraisal is not a deal-killer. It’s a negotiation trigger. In the current Austin market, the leverage is yours.

Frequently Asked Questions

Who pays for the appraisal in Texas?

The buyer pays, typically $400–$600 in Austin. Even though you’re writing the check, the appraiser is hired by your lender and works to protect the lender’s collateral — not to advocate for the value you agreed to pay. That’s an important distinction when the number comes back lower than expected.

Can I get my earnest money back if the appraisal comes in low?

Yes, in most cases. The Third Party Financing Addendum in standard Texas TREC contracts gives you a financing contingency. If the home doesn’t appraise at the purchase price and you terminate the contract within the financing deadline because you cannot secure financing on the original terms, you’re generally entitled to your earnest money back. Don’t wait — the termination must happen before the financing deadline expires.

What is a Reconsideration of Value and does it actually work?

A Reconsideration of Value is a formal request, submitted through your lender, asking the appraiser to review their conclusion in light of additional comparable sales evidence. It works best when there are legitimate comps the appraiser genuinely overlooked. Appraisers are not required to revise their values, and most do not. Your agent can evaluate quickly whether the comparable data makes a strong enough case before you spend the time pursuing one.

How common are low appraisals in Austin in 2026?

More common than most buyers expect. Travis County median home values are down 15.91% from their May 2022 peak. Appraisers use recent sold comparables to set value — and in a market where prices have corrected significantly, homes priced at optimistic figures are the most vulnerable to coming in low. It doesn’t mean the property isn’t worth buying. It means the seller’s price may not match what the lender’s data supports.

Should I still buy the home if the appraisal comes in low?

It depends on the size of the gap, your cash reserves, and how much you want that specific property. A $5,000 gap is a very different conversation than a $40,000 gap. In Austin’s 2026 buyer’s market, sellers know what the alternative looks like — losing a buyer and relisting into a 54-day average DOM environment — and a price reduction to the appraised value is often the most logical outcome for everyone. Your agent can help you decide which option fits your situation best.

Ready to Talk Through Your Options?

A low appraisal isn’t the end of the deal — it’s the start of a negotiation. In Austin’s current buyer’s market, the data is on your side, and the right agent makes all the difference in how that conversation goes.

The Muñoz Group negotiates appraisal gaps for buyers across Austin every week. If you’re under contract and the appraisal just came in low, or you want to understand your position before making an offer, we can walk you through exactly what to expect.

About the Author

The Muñoz Group at Compass is an Austin-based real estate team with 600+ transactions and $675M+ in career sales across Austin and 18 surrounding communities. Led by Group Principal and REALTOR® Lisa Muñoz, the team delivers a luxury experience at every price point, no matter where you are in your real estate journey. Learn more at munozaustin.com.